Economics is a type of discipline which studies the economic activities and undertakings of individuals living in societies, regions, countries, or the world as a whole. In economics, the effect of policy changes on the growth path of the economy over time is discussed. Therefore this section deals with some major key concepts of economics.

In the ordinary sense or normal thinking, economics is all about how to make money or manage money. This is not true as economics is much broader in scope. It is about choosing a state of scarcity. If the thing were not inadequate, there would not be a subject matter like economics, because then an individual or a nation could have anything that it wanted.

In reality, this not the case, and at least time are scarce. The richest person in the world today, Jeff Bezos, has to choose on a particular morning whether to do yoga for one hour or to have a video conference with the top executives of Amazon to talk about business policies or anything else relating to their business.

It is not only time but almost everything is inadequate in the sense that it is not always available freely. The degree of scarcity may vary from place to place or from nation to nation. For instance, in a developed country, labor is relatively scarcer than technology and equipment and in a developing country, it is just the opposite.

Every participant of the economy has to face the problem of scarcity and choice almost every time in their life due to the existence of scarcity of resources. The study of such problems faced by individuals, societies, nations, regions as well as at the global level is called economics.

In alternative words, economics is, therefore, the study of how society manages its scarce resources. Therefore, economics does study how individuals make decisions; how much time they prefer for work and leisure or entertainment, how much they buy and what they buy, what factors affect their buying decisions, how much they earn, how much saving they prefer, and how they invest their savings and so on.

In economics, we also study how people interact with one another. For example, economics examines how buyers and sellers of goods together determine the price at which the good is sold and the quantity that is sold. And economists also analyze the forces and trends that affect the economy as a whole, including the growth rate of output, the rate of the population that cannot find work, the rate at which price is increasing, and so on.

A brief view of key concepts of economics

Some major key concepts of economics that have developed and identified the nature and definitions of economics are discussed as below;

Good and Bad

Economics speaks regarding goods and bad. In economics, good can be defined as anything which produces or generates utility or satisfaction to a person. For example, a laptop, a television set, friendship, and love. So good could be tangible and intangible. Thus, anything that could be good in economics has to ensure some satisfaction or utility to someone.

On the other side, a bad is something which gives an individual dissatisfaction or disutility. For example, coronavirus gives us dissatisfaction or disutility then we can call it bad. If the constant irritation of a friend is something that may give us disutility or dissatisfaction, then it is called bad.

All the people want good but they don’t want bad. People pay out of their resources only for attaining utility and which they only can get from goods.

We have certain things in our surroundings that are good as well as bad. There may be a case in which something is good for one person and bad for another. For example, smoking cigarettes give some people satisfaction and other dissatisfaction. So we can say that smoking cigarettes can be good for some people and bad for others.

Resources

It is one of the most important key concepts of economics. The resource is anything that is regarded as a source of supply that contributes to producing something. Generally, term resources signify materials, energy, services, staff, knowledge, or other assets that are transferred to produce benefit and in the process may be consumed or made unavailable.

Benefits or resources utilization may include an increase in wealth, meeting human needs or wants, proper operation of a system, or enhance overall well being.

We use several types of goods and services in our daily life and they do not just appear before us we snap our fingers. They take resources to get the final shape. So we can say that inputs to produce something are resources and sometimes we call them a factor of production.

Generally, economists divide all the resources into four broad categories; Land, Labour, Capital, and entrepreneurs.

- Land (Land includes all gifts of nature to the living beings including soil, forest, Himalaya, water, air, etc. they are free, passive, and fixed in supply)

- Labour ( it refers to the mental and physical efforts of human beings to perform a particular task, supply based on the wage rate, and demand based on MPL)

- Capital ( Manmade objects used in further production and they add further values on goods and services, capital goods have a lifetime, elastic supply, and passive factor of production. Some examples of capital include factories, machinery, tools, computers, buildings, and so on.)

- Entrepreneur ( it is the team of risk-taker individuals having an intellectual ability for organizing and managing resources like land, labor, and capital to produce goods, see new business opportunities and expand a novel technique of undertaking things)

Scarcity

It is the condition of having greater wants in comparison to the limited resources like land, labor, capital, and entrepreneurship which are accessible to please those desires.

Alternatively, we can put the term scarcity as the case in which people are demanding goods and stuff but they don’t have sufficient resources to meet all their desired quantity of goods.

Wants that we have are always in unlimited magnitude, but the resources which are needed to produce pieces of stuff are always in a fixed volume. Thus, scarcity is the outcome of an individual’s unbounded wants beating in opposition to restricted resources.

Many economists declare that if scarcity didn’t stay alive, neither would economics. In other words, if our wants were not higher than the fixed resources available to meet them, there would not be the blind of knowledge called economics.

Thus in almost complete words, economics is the science relating to the study of people, societies, and nations as a whole to deal with the fact that needs are larger than the restricted resources accessible to please those wants. Scarcity affects everyone and everyone in the world has to face scarcity.

Scarcity tells us the story of human life’s reality and the importance of goods and commodities as well. It tells us how valuable goods are to human survival and growth.

The notion of scarcity may change along with the change in living standards and the lifestyle of the human being. But one thing is beyond sure that it always emerges and always exists in the life of human beings. The concept of scarcity was coined by British economist Lionel Robbins in the 1930s.

Choice

People have to make choices because of the problems of scarcity. The resources available to satisfy people’s wants are limited in supply. As most people cannot have all the goods and services they want, they have to make a choice. Since all desirable things are composed to satisfy our wants, we have to choose to make careful use of a scarce resource that is available at our disposal.

It means we have to economize the resources. Since resources are scarce, we must decide which want will be satisfied and which will not at a particular period, maximum satisfaction can be obtained by the utilization of available resources in a useful manner.

Thus, the problem of choice appears due to the greater demand for the resource than the supply of resources and applicability of available resources on various uses, i.e. alternative uses. If the resources had not embodied by alternative uses, the concept of choice would have arisen in human society.

Boundless wants and finite means create a problem of selection. Means have alternative uses and due to their alternative use we can fulfill important wants and postpone or give up less important. This is simply called a choice.

Benefit and costs

The relationship between benefit and cost also among some major key concepts of economics. No benefit comes without a cost. For example, we all want less pollution or a healthier environment. This is the case we are looking for benefits. But benefits can rarely be obtained without any cost. So eliminating pollution has benefits but it has costs as well.

For instance, one way to eradicate pollution from pollution making cars is to pass a law stating that anyone caught driving a car will go to prison for 4 years. If such a law passes and enforced then very fewer individuals will be able to run the car which is the cost of eliminating pollution. So it is something like my benefit is your cost and your benefit is my cost.

So economics always thinks everything in the form of cost and benefits both that noneconomic thinker may not think in the same way.

Decisions Made at Margin

Economic participants always decide on the margin. Taking anything additional or taking the decision to do or to take anything have cost as well as benefits. For instance, when deciding what to do, or not to do anything, economists consider that we have to think in terms of additional or marginal costs and benefits but not total cost and benefits.

Thus most of the decisions are based on additional change. Let’s take an example, suppose Robert just ended eating momo and drinking coca-cola for his lunch.

He is still a little bit hungry and is considering whether to order another plate of momo. Economists advise him to compare the additional benefits of the second plate of momo to its additional cost.

So we have to make a comparison between marginal benefit/marginal revenue and marginal cost. If marginal cost is greater than marginal benefit then Robert will not demand the second plate of momo.

Desire VS Demand

In a simple sense-desire and demand are similar things. But in economics desire and demand are different concepts and demand refers to something more than desire.

Desire refers to wishes to have something and in an ordinary term, demand is also a desire or wish to have some goods or services. In economics, the term demand has a more specific and special meaning. It is a strong desire which is backed up by ability.

It means any desire to turn into demand, the consumer should have money or resources to purchase (ability to pay) and he or she must be willing to pay (willingness to pay).

Therefore demand is the quantities of a commodity which consumers are willing to purchase at various prices during a given time. Willingness and ability to pay are thus essential elements for converting any desires into demand.

According to Prof. Marshall, “Demand refers to the quantities of a commodity that the consumers are and willing to buy at each possible price during a given time, other things being equal.”

From the definition it can be seen that several indispensable apparatus are mandatory to have demand in the economic sense and these are enlisted as;

- The desire for a good or service,

- Willingness to pay (the person who has such desire should have an enthusiasm to pay),

- Ability to pay (the person who has such a desire must be able to afford the price of the product),

- Price of the product or service (unascertained price is not able to create demand but for a desire, price is not necessary),

- Time (Particular time should be given),

- Quality of the commodity (The willingness to pay is affected by the quality of the goods and thereby the demand too)

Thus, only if the consumer has all these elements (desire, ability, and willingness) and availability of the desired goods or service then it becomes a demand.

Demand VS Desire

| Desire | Demand |

| The consumer may desire everything regardless of his or her ability to afford it. | The consumer should have all the elements to have a demand. |

| It is simply a wish to have something | It is a wish supported by ability, willingness, and availability. |

| Resources or money is not needed to have a desire | Resources or money is necessary to have a demand. |

| It has a wider scope or it is boundless | It is limited by resources, price, and availability. |

| Desire may take place anywhere and anytime. | It is related to a particular time and place. |

| A desire may not be fulfilled. | A demand may be fulfilled. |

| Having the desire is not sufficient for economic progress and the betterment of life. | Having demand is a stimulus for economic expansion and fulfillment of demand is base for the betterment of life. |

Efficiency

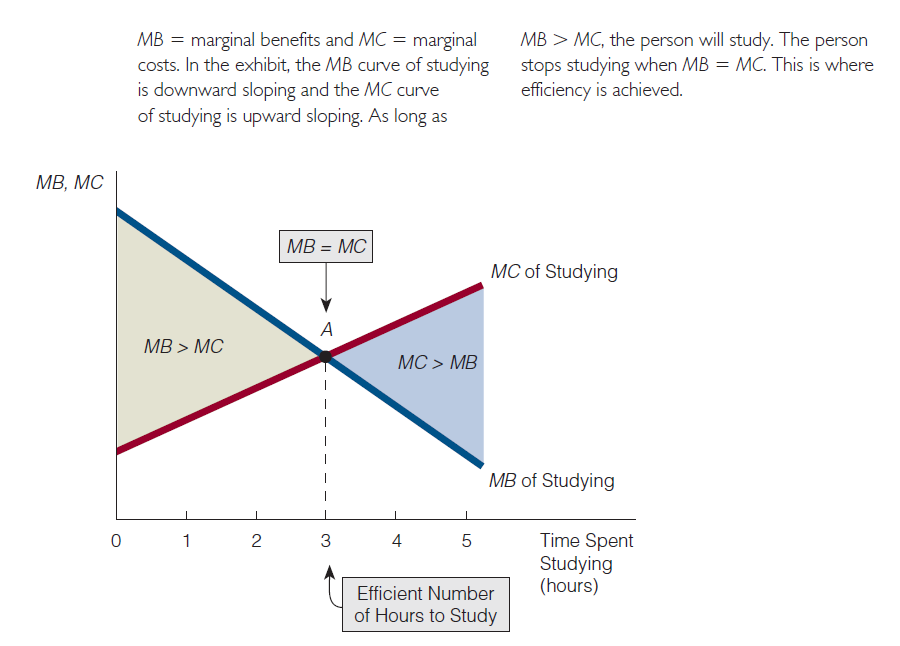

In economics, the right amount or quantity of anything is called an optimal or efficient amount. Generally, the condition having marginal benefit exactly equals to marginal revenue is called efficient outcome or efficient decision. So anyone can achieve efficiency when he has got his marginal cost is similar to marginal revenue.

Suppose one individual is studying for a test, and for the first hour of studying the marginal benefit is greater than the marginal cost. So he studies for the first hour because the time is providing higher benefit in comparison with marginal cost and he finds studying for an hour is worth it.

Again suppose for the second hour of studying, the marginal benefits are still higher than the marginal costs. He will again study for the second hour as well.

In this way, he will continue to study until he will find marginal benefits arrived from studying are less or equal to marginal costs incurred by studying. The following graph shows the concept of efficiency;

The above figure shows that the marginal benefit curve slopes downward assuming that the benefits of studying for the first hour are greater than that of the second hour and benefits from the second hour of study are higher than that of the third hour and so on.

On the other side, the marginal cost of studying is upward sloping indicating that the cost of studying the second hour is greater than the cost of studying the first hour, and the cost for studying the third hour of study is higher than the cost of studying the second hour. If we assume that the marginal cost per hour remains constant then the marginal cost curve will be a horizontal line.

The figure also shows that the marginal benefits of studying are equal to the marginal costs of studying at three hours of studying. So in our case, three hours of study is an efficient duration of time to study. Less than three hours show higher benefits and more than three hours show a higher marginal cost. So at three hours of study benefits is equal to marginal costs.

How to maximize the net benefit

The net benefit can be maximized by taking more of the units until the marginal benefits from such an additional unit will become equal to the marginal cost to the units. In our above case, studying up to three hours maximizes the net benefits to the student.

So economics teaches how to maximize the net benefit or gives an idea to maximize the satisfaction at a given amount of resources. This is the most important key concept of economics/microeconomics.

These are some major key concepts of economics or basic concepts of economics that have created and framed the entire subject matter.