Introduction of Monetary Policy and its Formulation in Nepal

The article aims to present the highlights of the Monetary Policy of Nepal 2020. Monetary policy is one of the tools that a national government uses to influence its economy. Using its monetary authority to control the supply and availability of money, a government attempts to influence the overall level of economic activity in line with its political and economic objectives. Usually, this goal is ‘macroeconomic stability’ that is low unemployment, low inflation, economic growth, and a balance of external payments.

Formulation and implementation of monetary policy is the major function of Nepal Rastra Bank. NRB Act, 2002 provided a clear legal and institutional framework for monetary policy. The monetary policy operating procedure was changed in response to the evolving needs of the time.

The formulation of monetary policy in Nepal formally received its institutional, legal, and more transparent framework in recent decades only. NRB Act, 2002 broadly provides the guidelines and institutional set-up for a monetary policy decision. It mandated the annual announcement of monetary policy by incorporating the review of past policy, programs for the following year, and the rationale for such programs.

NRB began the practice of formally announcing and publishing monetary policy statements starting from fiscal year 2002/03 which was a breakthrough in modernizing monetary policy through a more transparent framework with public dissemination. The overall monetary policy covers financial and foreign exchange policy as well.

By following the same Nepal Rastra Bank on Friday, July 17 has issued the monetary policy for the fiscal year 2077/78. The Highlights of Monetary Policy of Nepal 2020 is in the following sections.

Monetary Policy of Nepal 2020- Highlights

Economic Outlook

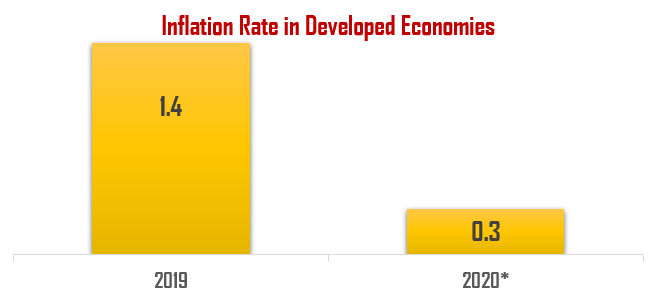

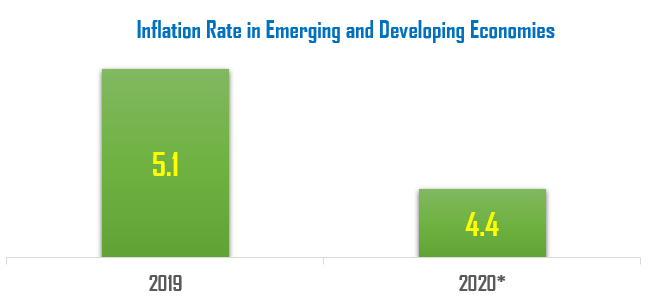

Global Economic Outlook

The attached photos show the global economic outlook.

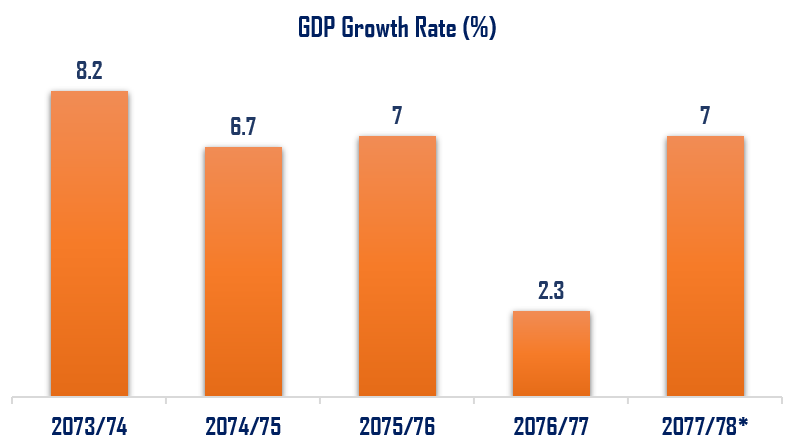

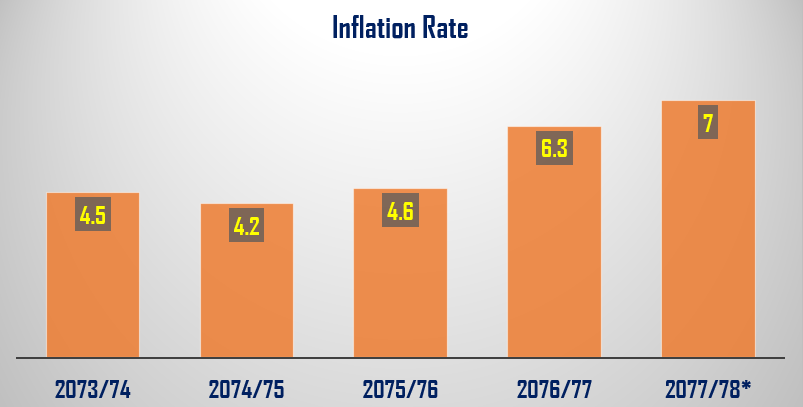

National Economic Outlook

The attached photos show the domestic economic outlook.

Monetary Policy Direction

- Monetary Policy emphasis to help the Government of Nepal to achieve its economic growth goals while maintaining macroeconomic stability.

- Financial mobilization will be encouraged to expand economic activities, create employment, and promote sustainable economic development.

- Liquidity will be managed to keep in view the pressure on price and external sector stability.

- Emphasis on the integration and strengthening of banks and financial institutions for the development and sustainability of the financial sector.

- Financial access and quality of service will be enhanced through the development of financial infrastructure.

- Electronic payment transactions will be encouraged by making the payment system efficient, robust, and secure.

Economic & Monetary Target

- Monetary policy has targeted to keep the inflation within 7%,

- Foreign exchange reserves will be maintained to cover imports of goods and services at least for 7 months,

- Growth of Private Sector Credit and the Broad Money Supply (M2) is aimed to limit at 20 % and 18 % respectively.

- Keeping economic recovery at priority, the monetary policy aims to maintain liquidity to help to achieve the goal of economic growth.

Operating Targets and Instruments

- The interbank rate of commercial banks has been the target of monetary policy, but now the weighted average interbank rate of commercial banks, development banks and finance companies will be taken as the operating target of monetary policy.

- The upper limit/ceiling rate (Permanent Liquidity Facility Rate) of interest rate corridor is set at 5% as it is and the lower limit/floor rate (Deposit Collection Rate) is decreased from 2 % to 1 %.

- Repo (which is also known as Policy Rate) reduced from 3.5 % to 3%.

- The mandatory Cash Reserve Ratio (CRR) remains at 3 % for all the BFIs.

- The Statutory Liquidity Ratio (SLR) is set 10, 8, and 7 % for Commercial Banks, Development Banks, and Finance Companies respectively.

- The Bank Rate, applied for the lender of last resort (LOLR) facility is kept at 5 %

Credit Management

Agriculture Sector Credit

- To revive the economy, credit investment in agriculture, energy, tourism, and domestic, small, and medium enterprises will be encouraged.

- Commercial Banks should disburse at least 15% of the total credit investment to the agricultural sector by Asar 2080.

- The Agriculture Development Bank will be developed as a leading bank in the agricultural sector, and the bank will be able to issue agricultural bonds,

- And the ‘Kisan Credit Card’ will be provided through the Agriculture Development Bank.

Energy Sector Credit

- To promote energy self-reliance, commercial banks should invest at least 10 percent of the total loan in the energy sector by Asar 2081.

- Commercial banks with investment experience in the energy sector can issue energy bonds.

- If a project starts exporting electricity, banks and financial institutions will have to give loans to the project by adding only 1 percent to the base rate for 5 years after the start of export.

Tourism Sector and Cottage, Small and Medium Enterprise Credit

- Priority will be given to various service-oriented businesses (which are most affected by COVID-19) such as transport, hotel, restaurant, aviation business, etc., in the flow of various concessional loans and refinancing facilities.

- Commercial banks have to disburse at least 15% of their total credit to the cottage, small and medium sector enterprises in the form of loans of less than Rs. 10 million by Asar 2081.

Concessional loan

- Provision has been made for commercial banks to disburse at least 500 loans or a minimum of 10 loans per branch and national level development banks to disburse at least 300 loans or a minimum of 5 loans per branch.

- In view of the impact of the Corona epidemic on the economy, concessional loan programs for productivity growth, job creation, and entrepreneurship development will be simply implemented. Such loans will be provided by BFIs to the borrowers at the rate of 5 percent in the specified areas.

- By Asar 2081, the Development Bank should disburse at least 20 % of the total loan and the finance companies should disburse at least 15% of the loan to the specified sectors including agriculture, micro, cottage, and small enterprises, energy, and tourism sector.

Real Estate and Housing and Margin Loans

- The limit of Personal Residential Home Loan will be maintained at 60 %.

- The real estate loan limit should be maintained at 40% within the Kathmandu Valley and 50% elsewhere.

- Margin Loan limit on the stock has been increased up to 70% from previously mentioned 65%.

Economic Recovery Programs

Refinancing Facility

- Provision for refinancing up to 5 times of the available funds for refinancing.

- Provisions are also made for special refinancing at a 1% interest rate in specified areas such as export-oriented industries, refinancing at a 2% interest rate in the cottage, small and medium-sized enterprises, and general refinancing at 3% interest rate in specified areas. In such refinancing, the borrower pays only 3%, 5%, and 5% interest respectively.

- The limit of lump sum refinancing given to banks and financial institutions has increased. Per person domestic and small enterprise refinancing limit of Rs 1.5 million, special and general refinancing limit of Rs 50 million and consumer evaluation based refinancing limit of Rs 200 million have been fixed.

Provisions of Loan Related to Profession/Business Operation Which is Most Affected by COVID-19

- Depending on the need of the borrower and the feasibility of the project/business to run the highly affected profession/business from COVID-19, the concerned banks and financial institutions will be able to disburse additional loan up to 20 percent of the current capital credit limit established in Chaitra 2076 BS.

- Banks and financial institutions will be provided criteria based loans at a 5% interest rate to re-operate, sustain and help in paying the remuneration of employees engaged in the businesses including tourism, cottage, small and medium scale enterprises, and other businesses affected by Corona, and similarly to provide entrepreneurial opportunities to those who are ruthlessly affected by the pandemic, through the mobilization of Rs. 50 billion funds to be established as provided in the budget of fiscal year 2077/78.

- Provisions are made for the borrowers to get the facility to extend their loan installment and interest payment period by 6 months to 24 months based upon the nature of the harshness of the COVID effect on different loaned sectors.

Financial Sector Reinforcement

- To reduce the risk by strengthening the capital base, the merger, merger, and acquisition process of commercial banks will be further encouraged.

- Arrangements will be made to merge the institutions that are directly / indirectly owned and controlled by the same family and business group and have established business relations with the same person or group.

- Mergers and acquisitions of MFIs will be encouraged to reduce the risk by strengthening the capital base.

Regulation and Supervision

- The credit to core capital plus deposit ratio (CCD Ratio) will be increased from 80% to 85%.

- Banks and financial institutions will be allowed to declare and distribute cash dividends up to 30% of the net distributable profits of 2076/77. However, if the net distributable profit is less than 5% of the total paid-up capital, the cash dividend cannot be distributed.

- The deadline for commercial banks to issue debentures at least 25% of their paid-up capital by Asadh 2077 has been extended to Asadh 2079.

- From the Fiscal Year 2077/78, the provision of Basel-III will be implemented in the national level development banks.

- Modify the stress testing guidelines of banks and financial institutions and bring them in line with international standards.

Microfinance

- The licensing of microfinance institutions has been postponed. Similarly, the licensing process of the organizations in the licensing process has also been cancelled.

- One year’s time limit has extended to transact at the state level for that microfinance which has registered to operate its functioning at the particular state only.

- The credit limit provided by microfinance is extended from Rs. 7 lakhs to Rs. 1.5 lakhs and the maximum interest rate charged to the customer is kept at 15 percent.

Payment System

- All types of financial transactions within Nepal will be encouraged to be done electronically and a national payment switch will be set up to facilitate this.

- Postponement of new permission to open a payment service operator or a payment service provider except previously agreed,

- Provision has been made to revoke the permission of PSP service providers if they will not reach at least 300,000 customers and if the average monthly turnover does not reach at least 600,000 by 2078.

- Guidelines will be issued to manage payments made through quick response (QR) code in electronic payments

- To manage the business of government bonds, government bonds will be dematerialized in coordination with the concerned agencies.

Foreign Exchange Management

- Following the provisions of Documents against Payment (DPA) and Documents against Acceptance (DAA), the foreign exchange limit for import has been fixed at USD 50,000.

- While importing goods from third countries through drafts, the foreign exchange facility limit of up to USD 30,000 at a time will be increased to USD 35,000.

- The term of the letter of credit will be increased from 120 days to 180 days

- Encourage professional hedging work to minimize exchange risk associated with the investment of foreign currency.

Institutional Good Governance, Financial Literacy, and Customer Protection

- Zero tolerance will be adopted in compliance with the guidelines on institutional good governance.

- Given the need to maintain thrift due to the Corona epidemic, the arrangements related to the remuneration and facilities of high-ranking employees of banks and financial institutions and the Board of Directors will be reviewed.

- To make the service charges levied by banks and financial institutions on customers more systematic and transparent, commercial banks, development banks, finance companies, and microfinance companies can take service charges on loan approval only up to 0.75%, 1%, 1.25%, and 1.50% respectively.

- Penal interest, fee, or compensation will not be charged from the customer for extending the principal or interest payment due to COVID-19.

- As long as COVID-19 is in effect, no charge will be levied if the ATM card of one institution is used in the ATM of another institution.

- The Central Bank will set up a separate portal on its website for receiving and managing inquiries and suggestions related to the banking services of the general public.

Endnotes

The implementation of monetary policy is believed to revive the economy affected by the epidemic while maintaining overall economic and financial stability. Although the Covid-19 epidemic poses a challenge to the economy, it is felt that the door is open for opportunities to manage exports and promote electronic payment systems by boosting domestic production.

It is believed that with the increase in access to electronic systems, employment will be created and entrepreneurship will be developed by increasing the production of electronic instruments and devices. From the monetary policy of the Fiscal Year 2016/17, Nepal Rastra Bank has started the practice of reviewing the monetary policy on a quarterly basis and with this monetary policy has gained its momentum and dynamism and thus there is scope for time-related revisions.

The data information enclosed in this article is assembled by the Enotes World team and is absolutely for all our readers. However, we would like to say that the comprehensive study may be needed before taking any decisions on the matters enclosed hereby as we have enclosed only the Highlights of the Monetary Policy of Nepal 2020.

Click the link to download the Monetary Policy of Nepal (in Nepali) for FY 2077/78.

NRB (2020). Monetary Policy of Nepal. Retrieved from https://archive.nrb.org.np/ofg/monetary_policy/Monetary_Policy_(in_Nepali)–2077-78_(Full_Text)-new.pdf

IMF (2020). World Economic Outlook Update, June 2020. Retrieved from https://www.imf.org/en/Publications/WEO/Issues/2020/06/24/WEOUpdateJune2020?fbclid=IwAR0T9KPN3XIVV4DY8j4kvMRDPPySiozA-RkZ4NaIwnteZT_LGuWhAdrBvSU