Introduction

The demand and supply curve let know us about different quantities of goods that are demanded by the consumers at various prices, and quantities that producers are willing to produce and sell at various prices respectively. But studying and knowing demand and supply will not tell us the actual price of goods in the market. So the important issue now is how we know the price of the product in the market. When consumers buy goods and business firms sell goods, they interact in the product market and the prices of goods and services are determined by the forces of demand and supply. The study of such matters is related to the analysis of market equilibrium.

Equilibrium and Disequilibrium

The term equilibrium in general form is the state of balance. It indicates the situation where the forces working in opposite directions come to balance. It is the position where there is no tendency to move or change unless there is a change in the forces influencing equilibrium. So it is the state of rest.

In the site of price determination, equilibrium refers to a situation in which the quantity demanded of a commodity equals the supplied quantity of the commodity. It deals with the balance between opposite forces of market demand and supply. Thus, in the competitive free market balance or equilibrium occurs when the quantity of demand and supply are equal to each other. The state of no equality between demand and supply is disequilibrium.

Equilibrium Price

It is a price at which the quantity demanded for a commodity equals the quantity supplied. At equilibrium, price, demand, and supply all three are in equilibrium. Equilibrium price clears the market-that the quantity supplied exactly equals to quantity demanded and there is no unsold stock of the goods.

Demand Side in Market Equilibrium

The demand side of the market equilibrium is related to consumers. Consumers do demand commodities because they possess utility-the power to satisfy human wants. Consumers are ready to pay a certain price for a commodity as it gives satisfaction to them. Here the consumers always would like to pay or scarify low as much as possible. The maximum price that a consumer is willing to pay for a commodity at a given time is equal to its marginal utility. The marginal utility does mean the additional utility added from the consumption of an additional one unit of the commodity. The marginal utility of the consumers will set the highest price that they would like to pay.

Supply Side in Market Equilibrium

The supply side is related to the producers. Producers supply products into the market to earn a profit. Thus they would like to charge a high price as much as possible. They have a minimum limit of price and below such; they cannot supply the product as there is something cost associated with the production of the product. Therefore they must get at least that much price which is equal to its marginal cost of production.

By looking at the demand as well as the supply side of the market equilibrium we can say that consumers and producers have opposite interests in the market. However, such opposite interests are reconciled in the market through the market forces of demand and supply. Thus the interaction point of these opposite behaving forces is called equilibrium. And the equilibrium price, therefore, is the commonly agreed price by the buyers and sellers. This price is determined somewhere between its minimum limit (marginal cost of production) and the maximum limit (marginal utility of consumers).

Thus, the equilibrium price is the price at which the consumers are willing to purchase the same quantity of a commodity that producers are willing to produce and offer to sell in the market. The quantity that is purchased and sold at equilibrium price is called equilibrium quantity and such a situation is called market equilibrium. Once such equilibrium is achieved at the equilibrium price, there is no tendency for the producers as well as consumers to move away from it. No one has an incentive or pressure to change the price or quantity consumed or purchased after attaining the equilibrium.

Determination of Market Equilibrium-An Illustration

In a perfectly competitive market, a single supplier cannot influence the market price and thus has no role to play in the price determination. Here the price is determined through the interaction of market demand and market supply. Thus, the market is in a state of equilibrium when the quantity supplied exactly equals the quantity demanded at a given price. The process of measuring the equilibrium price in a perfectly competitive market can be further explained with the help of the following table.

| Price (Rs. Per Unit) | Quantity Demanded (in Unit) | Quantity Supplied (in Unit) | Market Position | Effect on Price |

| (1) | (2) | (3) | (4) | (5) |

| 100 | 30 | 56 | Excess Supply | Decrease |

| 90 | 40 | 50 | Excess Supply | Decrease |

| 80 | 45 | 45 | Equilibrium | Stable |

| 70 | 55 | 35 | Excess Demand | Increase |

| 60 | 70 | 20 | Excess Demand | Increase |

The above table shows various quantities of the commodity that consumers are willing to buy (column-2) at various prices (column-1), and the various quantities of commodities that suppliers are willing to supply (column-3) at these prices. Here the consumers’ willingness to buy represents demand/market demand and is inversely related to prices. And the willingness of sellers to sell is market supply and that is positively related to the prices.

There is a single price (Rs.80), at which market demand and market supply are equal to each other. Therefore, Rs. 80 is the equilibrium price and equilibrium quantities of supply and demand are 45 units. All the other prices are disequilibrium prices as demand does not equal supply at these prices.

Here the question is why other prices are not equilibrium prices. Let us discuss the determination of the equilibrium price. Here at all the prices below Rs.80, consumers are willing to purchase a larger quantity than the sellers are willing to sell. Suppose at the price of Rs. 60 per unit the buyers are willing to buy 70 units of the product but the suppliers are willing to supply only 20 units of their product. Thus, quantity demand is more than quantity supply. The amount by which quantity demand exceeds the quantity supply is excess demand or shortage. In the case of excess demand or shortage, consumers are not getting what they wish to get and as a result, there will competition between buyers to get the limited quantity of product and producers will begin to ask for higher prices. Thus prices will increase in case of shortage or excess demand in the market. This will continue to happen until excess demand would become zero or until the market will again reaches the equilibrium point.

Now considering the prices beyond the equilibrium price, consumers are willing to buy smaller quantities and sellers are willing to supply higher quantities. For instance, at the price of Rs. 90 per unit, sellers supply 50 units of their output, and buyers only demand 40 units and as a result, there is an excess supply of the product in the market. This situation is a surplus situation. The amount by which the quantity supplied exceeds the quantity demanded is excess supply or surplus. In the case of a surplus, producers are not able to sell some of their products as there is lower demand in the market. This will lead to competition between sellers to sell their products at a lower price to attract more consumers. So consumers’ bargaining power will increase by seeing such products unsold in the market and ultimately it will reduce the market price of the product. This process will go continue until excess supply will become zero or until the market will get equilibrium again.

It is thus at any price above and below Rs. 80, there will emerge a situation of surplus and shortage respectively. So Rs. 80 per unit is only the price in which quantity demand equals quantity supply and there will not any tendency to deviate from that point.

Graphical Presentation of Market Equilibrium

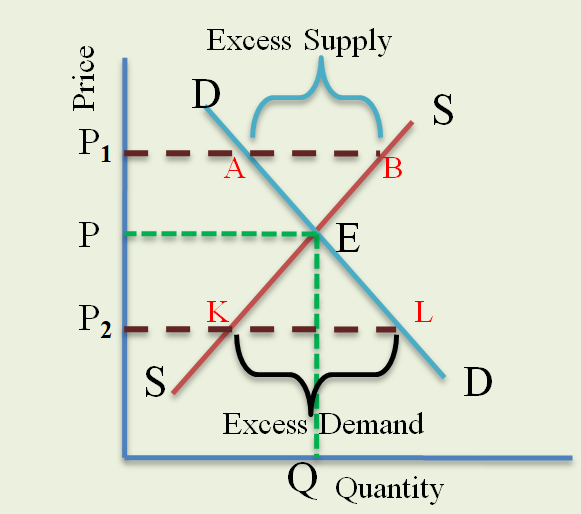

The measurement of equilibrium price and quantity in a perfectly competitive market can also be presented in the graph. The following graph shows the equilibrium price, demand, and supply at a certain given time.

In the above figure, DD is downward sloping demand and SS is an upward sloping supply curve. E is the equilibrium point where the demand curve intersects the supply curve and equilibrium price OP and equilibrium quantity of demand and supply OQ are determined. If the price increases to OP1, the demand decreases from PE to P1A. At higher prices, many consumers who could afford the OP price would not be able to purchase it. On the other hand, supply will increase to P1B as the supplier would supply more with a higher price to earn more profit. Such an increase in quantity supply and a decrease in quantity demand will generate a surplus of excess supply of the product in the market. The excess supply at price OP1 represents by AB in the figure. This AM amount of excess supply will force the sellers to reduce the price to attract, more consumers to dispose of their surplus stock. Ultimately this competition between sellers sooner or later will reduce the piece and the market will come back to the equilibrium position.

On the other hand, when the price decreases to OP2, the quantity demand will increase to P2L. Many consumers, who were not able to get the product at the higher prices, would start purchasing this commodity at a lower price. But the supply at such a price will decrease to P2K. Here the demand is greater than the quantity of supply and such a situation is a shortage of excess demand in the market. This means consumers are not getting their desired units of the product and this will create competition between them to get the limited quantity of products. In an attempt to get this commodity they are prepared to pay a higher price. Ultimately this will increase the price until the market will reach equilibrium. The adjustment between excess demand and excess supply ultimately invites the equilibrium price in the competitive free market. This denotes the situation of stable equilibrium.

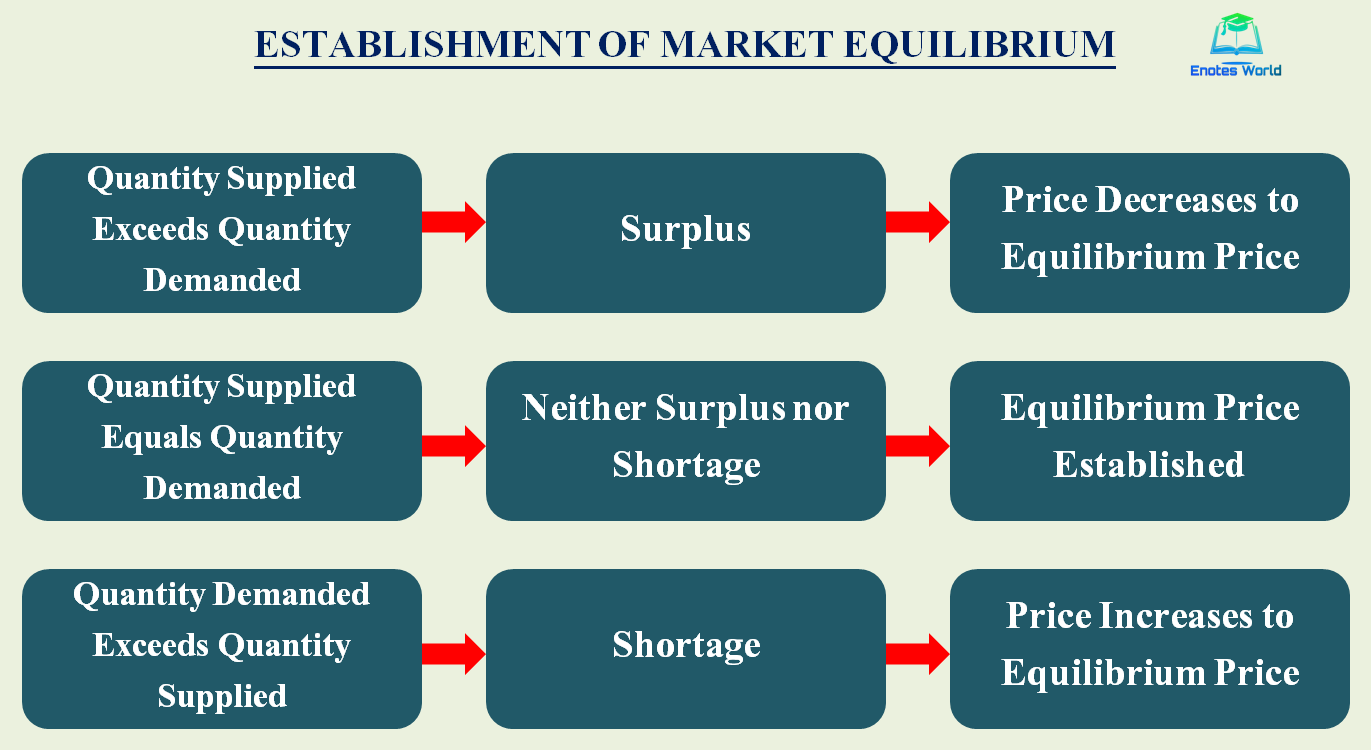

From the discussion, we can say that the price of a commodity in a perfectly competitive market is determined by the forces of demand and supply. It should be remembered that it is neither demand alone nor supply alone that determines the price of a product; both are necessary for determining the market price. In the summarized form of our discussion, the following chart shows the equilibrium establishment process in a perfectly competitive market.

References and Suggested Readings

Adhikari, G.M. (2012). Microeconomics. Kathmandu: Asmita Publication

Dhakal, R. (2019). Microeconomics for Business. Kathmandu: Samjhana Publication Pvt. Ltd.

Dwibedi, D.N. (2003). Microeconomics Theory and Applications. Delhi: Vikas Publishing House Pvt. Ltd.

Kanel, N.R. and et.al. (2016). Microeconomics. Kathmandu: Buddha Publication.

Koutsoyiannis, A. (1979). Modern Microeconomics. London: ELBS/Macmillan.

Mankiw, N.G. (2009). Principles of Microeconomics. New Delhi: Centage Learning India Private Limited

Salvatore, Dominick. (2003). Microeconomics: Theory and Application. Oxford University Press, Inc.

Shrestha, P.P. and et.al. (2019). Microeconomics for Business. Kathmandu: Advance Sarswati Prakashan.