Meaning of Equilibrium

The word equilibrium has been derived from the Latin word ‘aequilibrium’ which means equal and balanced. So the term equilibrium indicates the state of balance on or after which there is no tendency to shift. Just like other economic terminologies the term equilibrium also can be defined in various ways.

In modern economic theories, the concept of equilibrium has created the foundation and provided a guideline and direction to almost all economic theories.

Simply it is a gathering of certain interconnected variables in such a way that there is no inherent propensity to adjust or change from the prevailing situation or gathering in the model they consist of.

For an individual person, equilibrium is said to be attained by him or her when he or she assumed or recognized his or her concrete performance or behavior as the possible most excellent under the given conditions and he or she does not feel beneficial to change his or her actions and in such case, this excellent situation is called equilibrium.

The same is applied and holds true to define the equilibrium of a firm or producers and for the industry.

Thus equilibrium refers to the state accomplished by the individual, by the firm, or the industry, and from which they do not have any tendency to budge.

This thing can be seen from the consumer’s and producer’s viewpoints as well. From the perspective of an individual consumer, equilibrium will be attained when he or she gains maximum pleasure subject to income constraints or from the utilization of his or her known income exhausted on different products.

Similarly for an individual producing unit (firm or producer) equilibrium position will be obtained when he or she gains maximum profit subject to budget or resources constraints.

The industry will be known to attain equilibrium when all the business firms under the industry are in equilibrium and there exists no propensity to alter and adjust the size of the industry.

All the matter reveals the reality that an equilibrium position is that point or situation where one and all in the entire system assume that he or she can’t improve that particular situation a lot by varying its actions and behaviors.

Coming to the case of the market mechanism in a free market the situation called equilibrium would obtain at the point where the quantity of a particular good or service offered by its seller or producer is exactly equal to the quantity that the buyers of that particular goods or service want to purchase. At that point, three equilibrium values are determined equilibrium price, the equilibrium quantity of demand, and the equilibrium quantity of soles.

Let’s look at the concept with the following diagram;

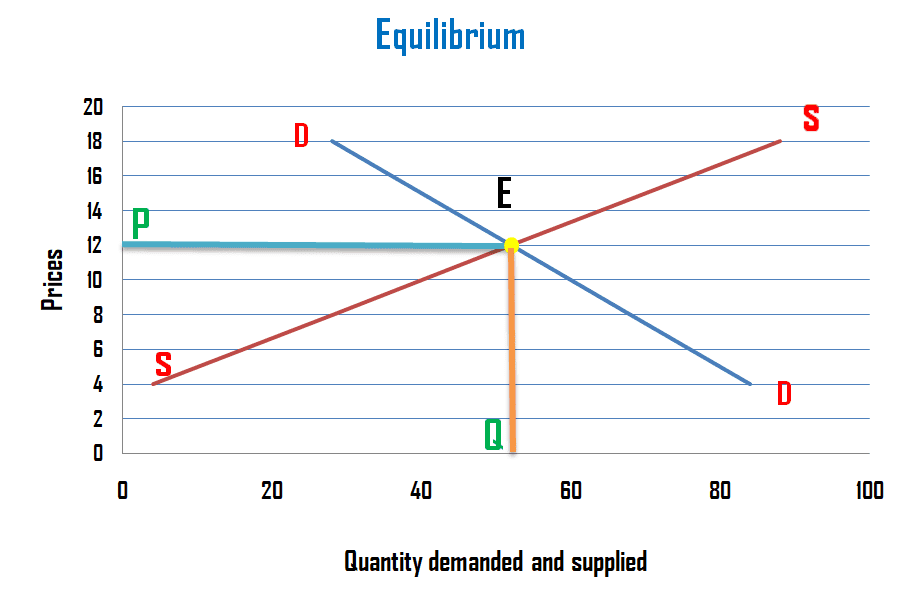

The X-axis measures the quantity demanded and supplied and Y-axis measures the price. DD is the demand curve. The demand curve shows the different consumers’ equilibrium points. It means at every point on the DD demand curve consumer attains equilibrium.

Thus, the demand line of the consumer is also known as the planning curve as it represents their maximum utility points at different prices. Similarly, SS is the supply curve in the market. Every point of the supply curve shows the producer’s equilibrium points. It means on the supply curve the producer can maximize his or her profit or minimize the cost.

‘E’ is the intersection point of DD demand and SS supply curve. At that point, the consumer’s equilibrium point and the supplier’s equilibrium point are coinciding with a particular market price. So the price that equalizes the demand and supply (consumer’s equilibrium point and supplier’s equilibrium point) is called equilibrium price.

The market is in the rest situation and known as market equilibrium. So equilibrium in the market is the situation where two opposing forces are in a balanced state. A positive quantity of demand, supply, and price is measured in the equilibrium situation in the market as OQ, and OP respectively.

Problems or Issues Linked with Equilibrium

The equilibrium discussed above may or may not exist. An issue that deals with whether equilibrium exists or not is the existence problem of equilibrium or the existence issue of equilibrium. Along with the existence problem, two other problems are also connected with equilibrium. These are the problem of uniqueness and stability of equilibrium.

All of these issues or problems can be best understood with the partial equilibrium analysis of market demand and supply. For such let us consider that there is a perfectly competitive product market having buyers and sellers of a particular product. Both of the participants (buyer and seller) are guided by their self-interest and motives as both are rational economic entities. So there is a demand as well as supply function in the market at different prices.

Existence of Equilibrium

The equilibrium we discussed above to exist requires some necessary conditions. It means equilibrium may or may not be existed all the time. So the necessary conditions for the existence of equilibrium are given as;

Both demand and supply schedules/curves must intersect with each other at a positive price.

It means equilibrium in economics existed in the first quadrant only. Demand and supply both are the functions of price so they must be equal at a positive price. Equality between demand and supply at a negative price does not make any sense in economics.

Having downward sloping demand and upward sloping supply schedules do not make sure that both will intersect and an equilibrium price will be determined.

Therefore there is no assurance that equilibrium will exist even when the demand curve is downward sloping and the supply curve is upward sloping. There can be situations when equilibrium does not exist at all even though the demand curve is downward-sloping and the supply curve is upward-sloping.

In the following cases, the equilibrium may not exist even though there is downward sloping demand and upward-sloping supply curves

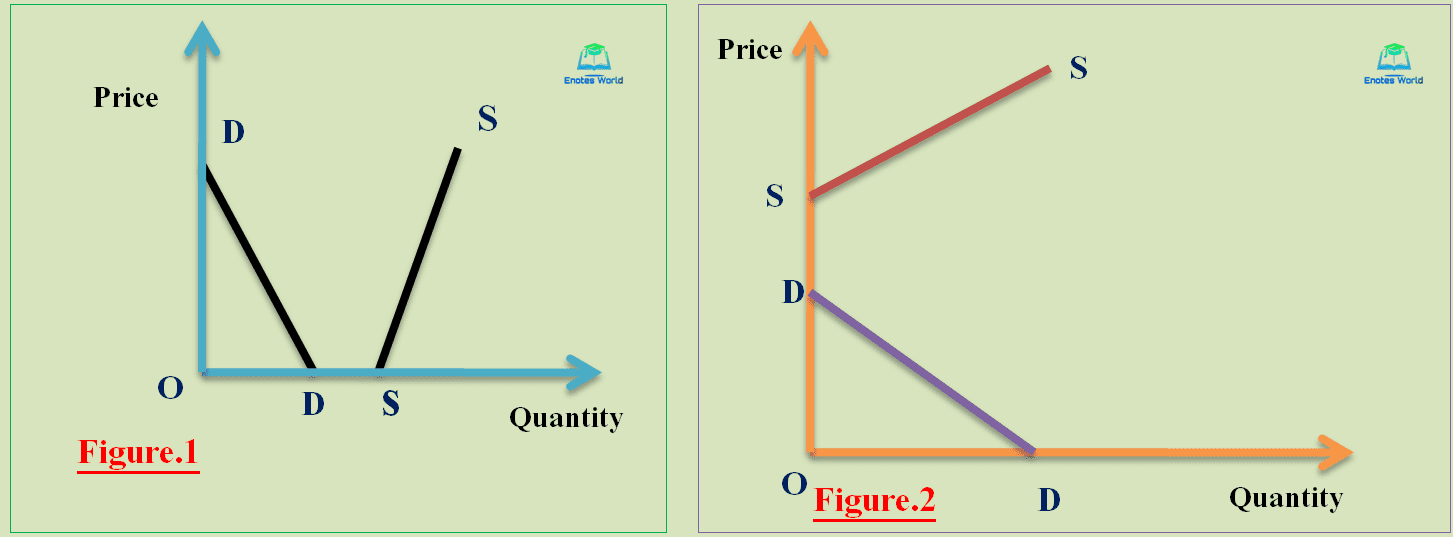

Case-1: If there is no positive price/case of a negative price/case of free goods. (Shown in figure 1 )

Case-2: If the minimum supply price is greater than the maximum demand price. (Shown in figure 2)

Both of the cases are explained with help of the following figures;

Figure 1 shows the case of free goods and the non-existence of market equilibrium. Figure 1 in the diagram shows that supply is greater than demand (excess supply) and it holds true in the case of free goods like air, and water. There is zero marginal cost of production so there is no price at all. It only applies in the case of freely available goods of nature such as clean air open space etc. However, this may vary over time. For example, clean air was free but the mounting industrialization and deforestation have pot now some social value or price on it although not a market price yet. So the concepts like Green GDP are becoming significant.

In the figure-2 we see the supply price is higher than the demand price. It means the price at which the seller can offer the product in the market is very high than the price at which buyers are willing to purchase. In the case of those goods which are very costly and have a very high marginal cost, the supply price would be higher than the demand price and no equilibrium would exist. For example, if a producer has to sell a gold car in the market. There may not be a demand for that car or very less demand due to a higher supply price. So in this case also equilibrium does not exist.

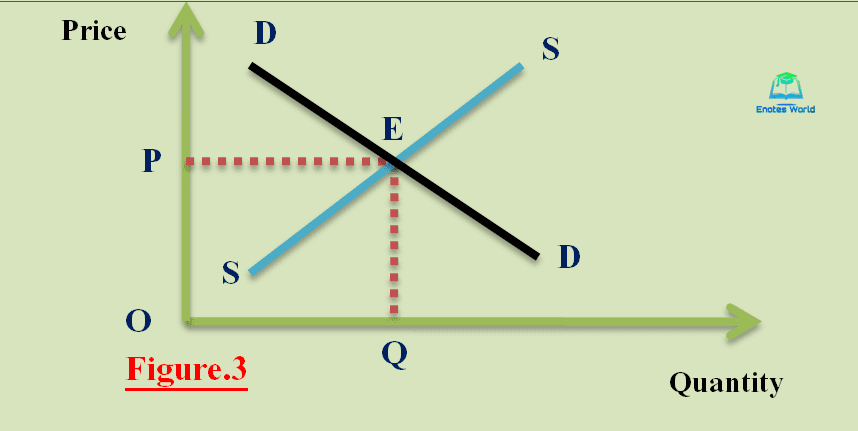

Case of Existence of equilibrium

So the only case of the existence of equilibrium is the interaction of the demand and supply curve at a positive price with positive quantities of demand and supplied as shown in figure 3.

Excess Demand Function Approach to the Existence of an Equilibrium

It is an alternative method of analyzing the existence problem of equilibrium. We use the excess demand function and its slope to identify the cases in which the existence of an equilibrium is possible.

Here, Excess demand EP = QDp-QSp (Gap between quantity demanded and supplied at a particular price)

Under the excess demand function approach, the equilibrium exists when the excess demand curve or function intersects the price axis with zero excess demand (neither excess demand nor excess supply, QDp= QSp). Also, the slope of the demand function at the intersection point with the price axis should be negative to be a stable equilibrium.

So necessary conditions are; excess demand curve or function must intersect the price axis with zero excess demand and the slope of the demand function at the intersection point with the price axis should be negative.

That intersected price would be an equilibrium price and at such an equilibrium price, there is neither excess demand nor excess supply. Or excess demand is zero at the equilibrium price.

At a price lower than the equilibrium price demand exceeds supply and hence excess demand is positive. If the price goes down continually then positive excess demand goes on increasing.

If the price goes beyond the equilibrium price then supply exceeds demand and hence excess demand becomes negative. As the price goes up continuously then negative excess demand also increases continually.

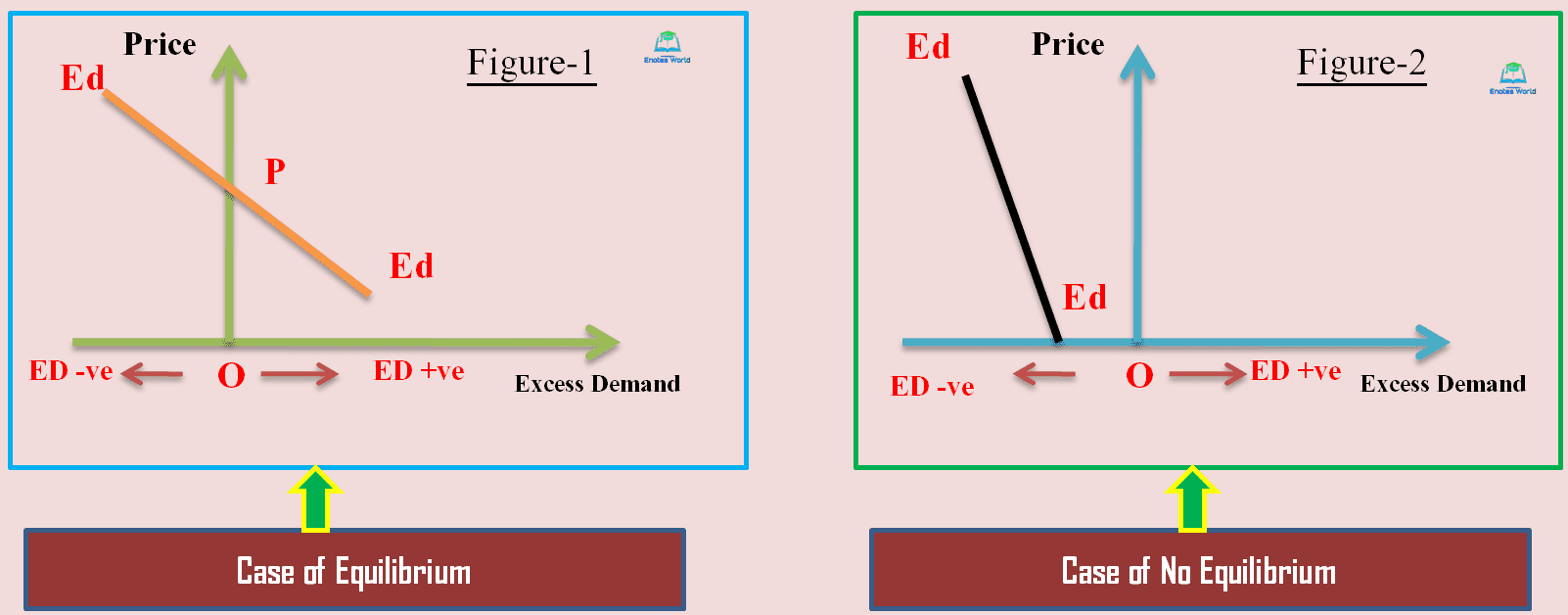

The case of the existence of equilibrium and non-existence of equilibrium under the excess demand function approach can be shown in the following diagram;

The excess demand curve is the function of price. So it is downward sloping. In figure-1 the excess demand function Ed has intersected the price axis at price OP (positive price) and there is zero excess demand (demand exactly equals supply). So in such a case, we can say that equilibrium exists in the market and there is equability between demand and supply in the market at the price OP.

In figure-2 there is no positive price when excess demand is zero. So there is no existence of equilibrium even though the excess demand is downward sloping. In the second figure even at zero prices, excess demand is negative so it must be a free good. So in the case of free goods, the equilibrium does not exist.

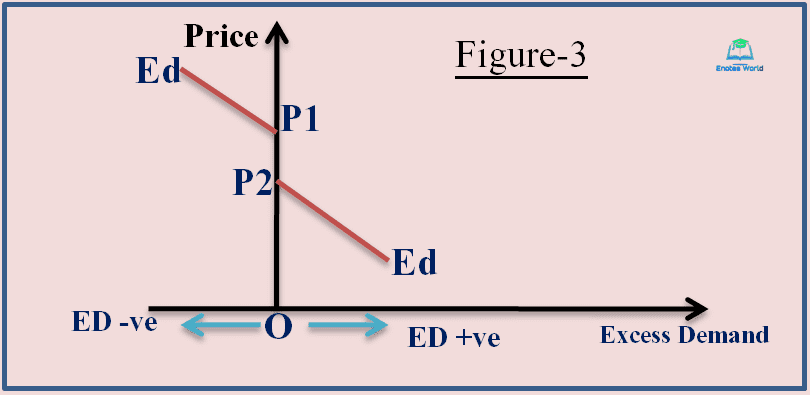

Case of Multiple Equilibria

In the case of multiple equilibria, equilibrium does not exist. The following figure-3 shows how the multiple equilibria do not ensure the existence of an equilibrium.

In the figure, between the price range, P1 P2 excess demand is equal to zero (market demand is equal to supply) for all prices. It means there are two or more equilibriums and that is called multiple equilibria. In the diagram beyond the price P2, there is no further demand and below the price P1, there is no further market supply. Therefore there is no possibility of equilibrium beyond the price P2 and below the price P1. The possibility of interactions of demand and supply is thus only between the price range P1 and P2 but there is no possibility of a single equilibrium.

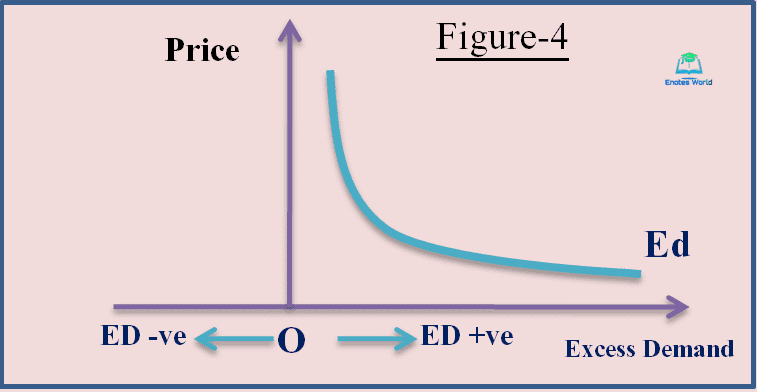

Case of Excess Demand Function as a Hyperbola

In the case of excess demand function as a rectangular hyperbole and located in the first quadrant there is no possibility of the existence of equilibrium. Figure 4 shows such a case.

At a very high positive price, the excess demand approaches near zero but never becomes zero. The excess demand function is an asymptotic curve and it comes closer and closer to both of the axes but never touches them. Thus, there is no possibility of the existence of equilibrium.

Therefore the problem of the existence of equilibrium is connected to the problem of whether the consumer’s and producer’s behavior ensures that the demand and supply curves intersect at some positive price. The only case of the existence of equilibrium is a positive quadrant with positive price, positive quantity demanded, and supplied.

Reference

Koutsoyiannis, A.(1979). Modern Microeconomics. London: ELBS/Macmillan